Thinking of Selling Your House? This is a Perfect Time!

Thinking of Selling Your House? This is a Perfect Time!

It is common knowledge that a great number of homes sell during the spring buying season. For that reason, many homeowners hold off putting their homes on the market until then. The question is whether or not that is a good strategy this year.

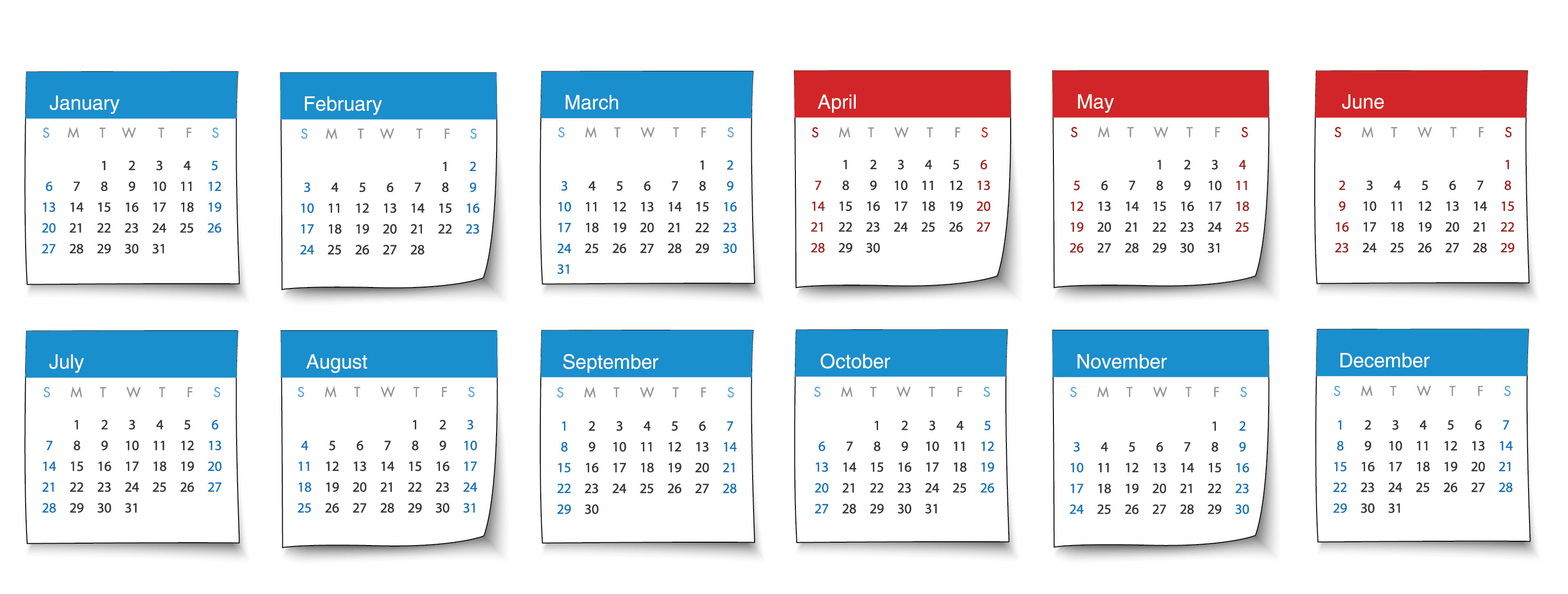

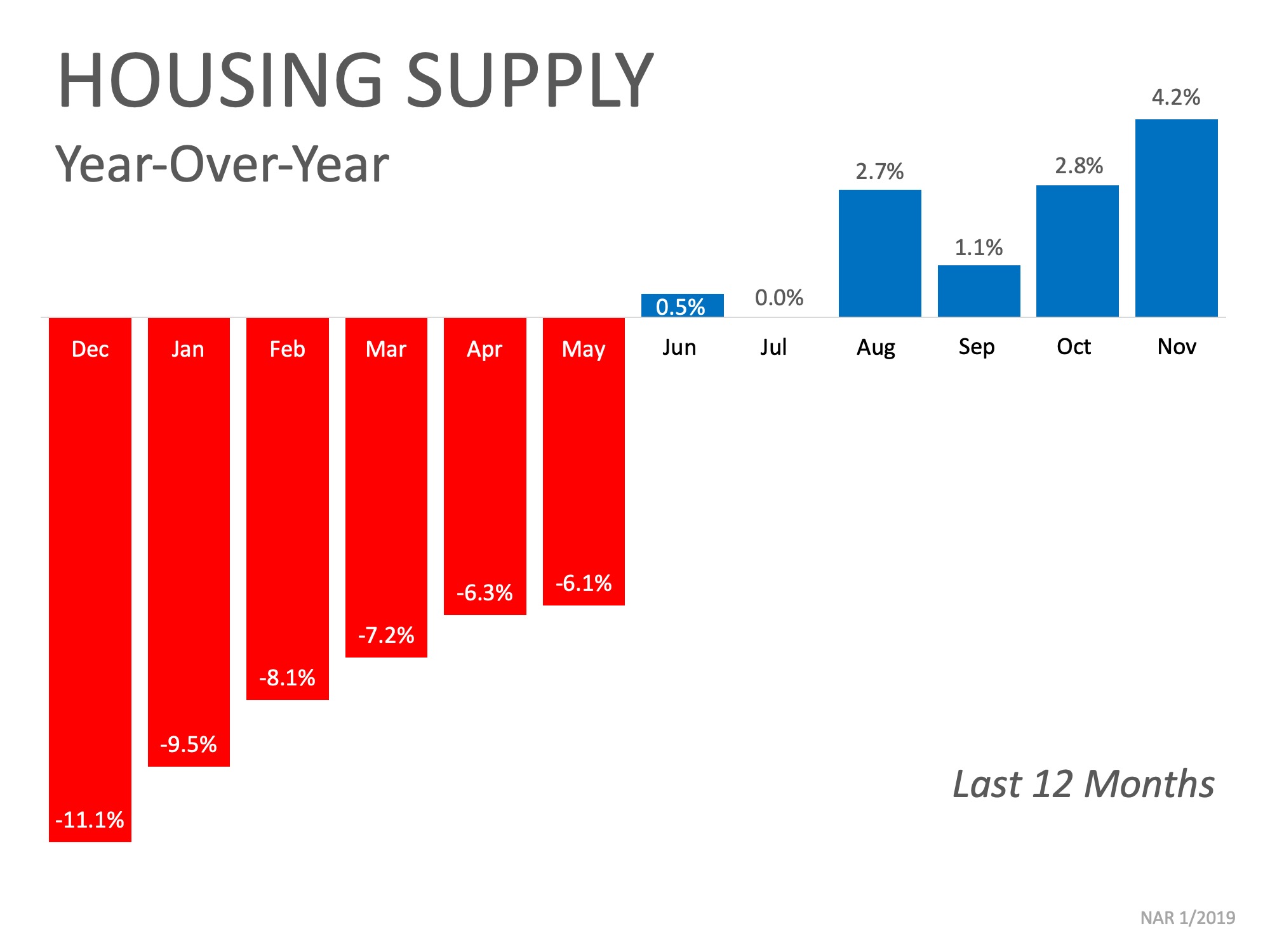

The other listings that come out in the spring will represent increased competition to any seller. Do a greater number of homes actually come to the market during this season in comparison to the rest of the year? The National Association of Realtors (NAR) recently revealed the months during which most people listed their homes for sale in 2018. This graphic shows the results:

The three months in the second quarter of the year (represented in red) are consistently the most popular months for sellers to list their homes on the market. Last year, the number of homes available for sale in January was 1,520,000.

That number spiked to 1,870,000 by May!

What does this mean to you?

With the national job situation improving and mortgage interest rates projected to rise later in the year, buyers are not waiting until the spring; they are out looking for homes right now.

Bottom Line

If you are looking to sell this year, waiting until the spring to list your home means you will have the greatest competition amongst buyers. Beat the rush of housing inventory that will enter the market and list your home today!

Christie Cannon | REALTOR

The Christie Cannon Team

Keller Williams Realty Frisco

972-215-7747

www.ChristieCannon.com

www.CannonTeamHomes.com

![Where is the Housing Market Headed in 2019? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2018/12/28075149/20181228-STM-ENG-1046x1354.jpg)

![Buyers Are Looking for Your Home, Now [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2018/12/20095142/20181221-STM-ENG-1046x808.jpg)