Real Estate News: November Home Sale Drops

The National Association of REALTOR has recently published their latest report on existing homes sales for November (likewise, they revised their October numbers). The most recent report Existing Home Sales offers that preowned home sales:

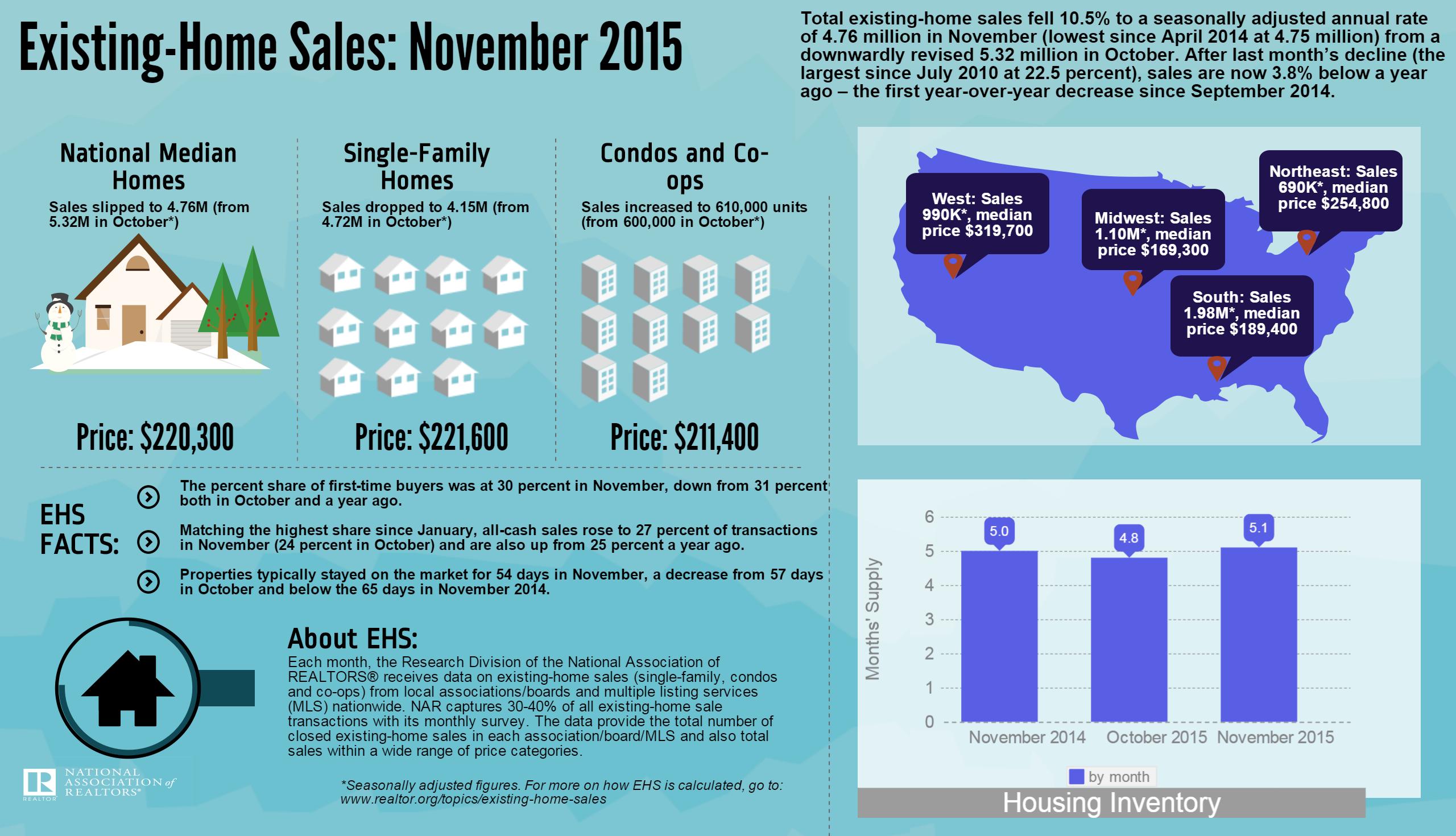

“…fell 10.5 percent to a seasonally adjusted annual rate of 4.76 million in November (lowest since April 2014 at 4.75 million)…” The report reflects that November was the slowest in 19th months for existing home sales. This was displayed in a 10.5% decrease in month-over-month sales.

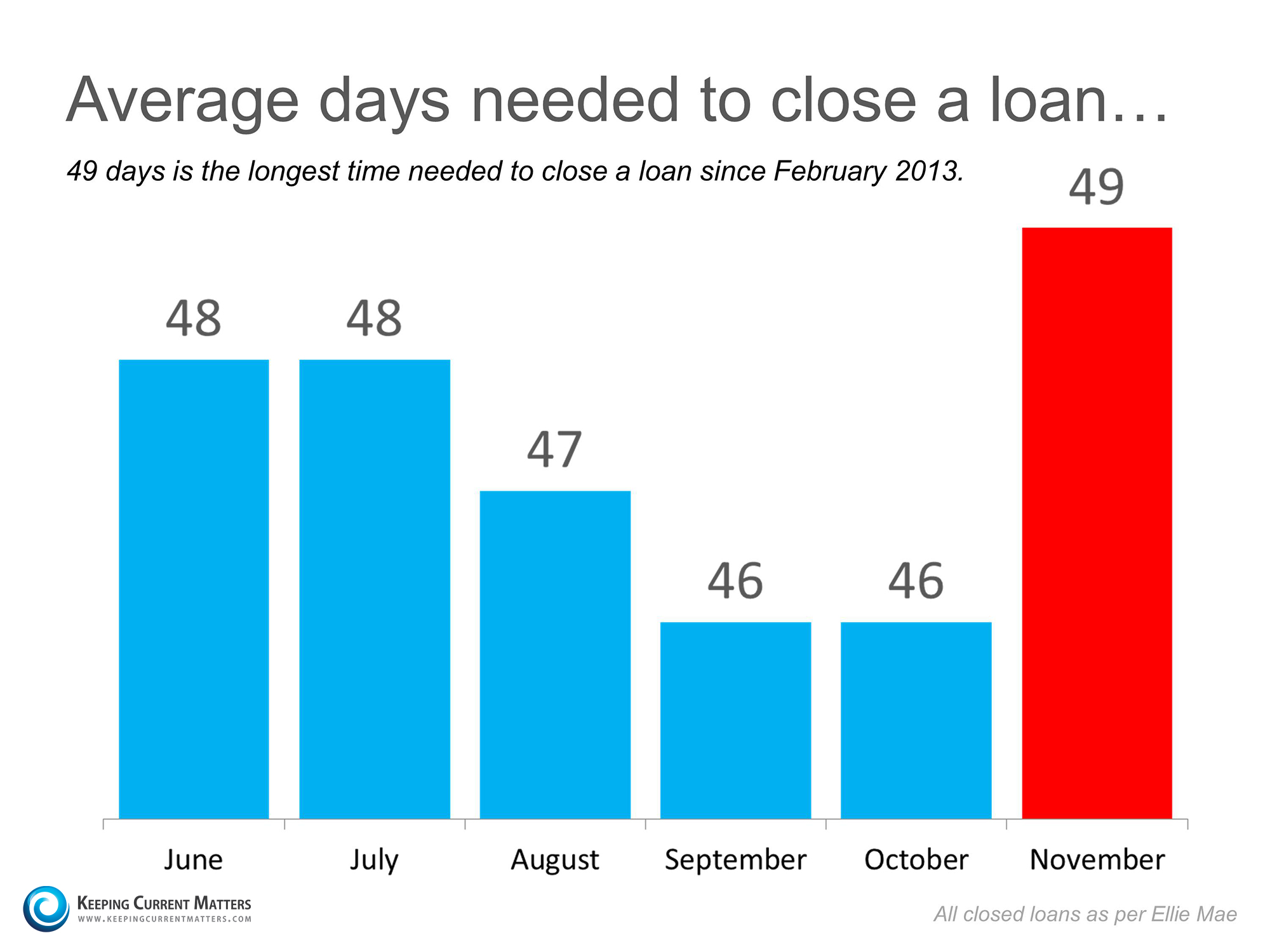

While there are still many hypotheses for the reasons of the drop, many industry insiders are placing a large portion of the blame on real estate’s adjustment to the latest changes in mortgage lending laws. With these adjustments, the industry has seen an overall increase in the amount of time it takes to close a traditional loan.

The numbers may seem miniscule on paper, the three day average increase reflects a whopping 15.7% of available banking days in November. Traditionally, most homes close in the last 3-days of the month, as such even a 2-3 day average increase “pushes” closings into the following month.

When we compare both written contract volume & anecdotal experience from the industry, most indications are that the sales are not lost. December reporting will be critical to see if the decrease was simply due to delay, or if November's numbers are a foreshadowing of a deeper market shift.

Christie Cannon - Keller Williams Frisco TX