Buying a Home Early Can Significantly Increase Future Wealth

Buying a Home Early Can Significantly Increase Future Wealth

According to an Urban Institute study, homeowners who purchase a house before age 35 are better prepared for retirement at age 60.

The good news is, our younger generations are strong believers in homeownership.

According to a Freddie Mac survey,

“The dream of homeownership is alive and well within “Generation Z,” the demographic cohort following Millennials.

Our survey…finds that Gen Z views homeownership as an important goal. They estimate that they will attain this goal by the time they turn 30 years old, three years younger than the current median homebuying age (33).”

If these aspiring homeowners purchase at an early age, the Urban Institute study shows the impact it can have.

If these aspiring homeowners purchase at an early age, the Urban Institute study shows the impact it can have.

Based on this data, those who purchased their first homes when they were younger than 25 had an average of $10,000 left on their mortgage at age 60. The 50% of buyers who purchased in their mid-20s and early-30s had close to $50,000 left, but traditionally purchased more expensive homes. Although the vast majority of Gen Zers want to own a home and are somewhat confident in their future, “In terms of financial awareness, 65% of Gen Z respondents report that they are not confident in their knowledge of the mortgage process.”

Although the vast majority of Gen Zers want to own a home and are somewhat confident in their future, “In terms of financial awareness, 65% of Gen Z respondents report that they are not confident in their knowledge of the mortgage process.”

Bottom Line

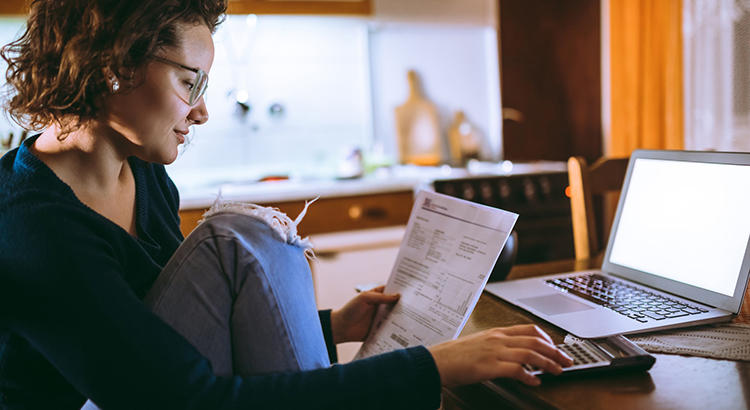

As the numbers show, you’re not alone. If you want to buy this year but you’re not sure where to start the process, let’s get together to help you understand the best steps to take from here.

![A Latte a Day Keeps Homeownership Away [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2019/08/22112914/20190823-MEM-1046x1308.jpg)

![Buying a Home? Do You Know the Lingo? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2019/08/13124327/20190816-MEM-1046x1354.jpg)