Article provided by: Swapna Venugopal Ramaswamy, USA TODAY

Exuberant buying – with multiple offers and bidding wars – has become common across the country, reminisicent of the fevered market before the 2008 housing crash.

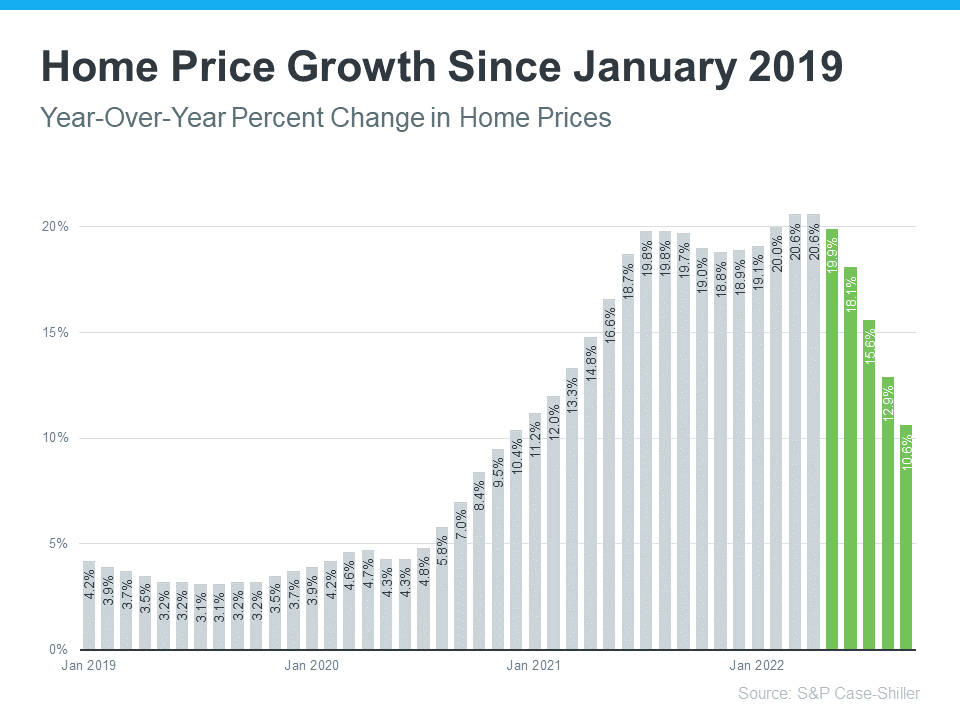

Home prices nationwide increased year-over-year by 18% in July 2021, the largest annual growth that CoreLogic Home Price Index has measured in its 45-year history.

That leads to the inevitable question: Will history repeat itself?

USA TODAY spoke to eight experts to find out if a housing crash is on the horizon.

The short answer? No.

For one, they say the housing market in 2021 is not like the boom-bust cycle leading up to the Great Recession.

In the years before 2008, mortgage lenders made subprime loans to borrowers without verified income or adequate down payments while pushing risky loan products. This time, tough loan underwriting standards are the norm even with rock-bottom interest rates.

►Homebuying tips:3 families bought and sold homes during the pandemic's red-hot market. Here's what they learned.

►Rent or buy?: That depends on where you want to live

On the supply side, a decade of underbuilding of homes, regulatory barriers, high construction costs combined with people staying longer in their homes have kept housing inventory low.

When it comes to demand, buyers’ desire for more space during the pandemic, low mortgage rates, rising savings, an improved labor market and millennials reaching their peak homebuying age have contributed to the tightening of the inventory.

But… home price growth will decelerate in the coming year, experts predict.

Stronger mortgage market

In the mortgage market of 2006, there was a proliferation of high credit risk mortgage products, while about one-third of all mortgages were low or no-documentation loans or subprime loans, says Frank Nothaft, chief economist for CoreLogic.

“It was a complete erosion and deterioration of credit underwriting standards in the economy, in the mortgage market,” he says. “The no-documentation loans were commonly referred to as liar loans because you'd lie about your income, you'd lie about your employment, you’d lie about your financial assets.”

This time around, it is completely different, he says.

“We have high-quality mortgage origination standards, and so we don't have mortgage finance fueling home price growth today," he said.

Forbearance programs and the housing market

One of the lifelines for homeowners during the COVID-19 pandemic has been forbearance, an ability to skip or make smaller monthly payments on mortgages under the CARES Act.

That left homeowners with more cash for emergencies.

In May 2020, two months after the pandemic caused havoc in the economy, more than 4 million U.S. mortgages were in forbearance.

Currently, there are an estimated 1.6 million homeowners in forbearance plans, which will start winding down by the end of September, according to the Mortgage Brokers Association.

Given the strong housing market and price appreciation, banks are more likely to work with borrowers to restructure their loans.

Those who are not able to make the payments might decide to sell their homes and enter the rental market, says Jeff Taylor, managing partner at Mphasis Digital Risk, a technology and risk firm that consults with mortgage lenders.

“We are currently guesstimating about probably 8% to 10% will actually have to go through the foreclosure process,” he says. “And it’s going to be geographically spread out so it will not have a big impact on the housing market.”

Climate change shapes relocations:Here's what families are doing.

To put that in perspective, more than 11 million mortgages entered the foreclosure process between 2008 and 2012 – which included the Great Recession – according to the Federal Reserve Bank of St. Louis.

Two economies

“The pandemic caused much more economic damage to lower-wage earners than mid-and upper-tier salary types who tend to be homeowners more than renters,” says Jonathan Miller, a state-certified real estate appraiser in New York and Connecticut.

With a rapid runup in prices, homeowners have a record amount of equity at their disposal and unlike the mid-2000s, are not leveraged to the hilt, Miller says.

“They're not using equity like an ATM in their home -- like they did during the bubble -- because the economy is fundamentally better,” he says. “I anticipate more of a plateauing phenomenon," with home prices, he says, rather than "some sort of sharp correction.”

Millennial homebuyers

The most significant housing demographic patch ever recorded in history – roughly 32.5 million people between ages 27 to 33 – will be actively trying to buy homes through 2024, according to housing analyst Logan Mohtashami.

.jpg)